“An increasing number of providers will need to make significant changes to their funding model in the near future to avoid facing a material risk of closure.”

That is very much not the conclusion you want from the higher education regulator’s annual assessment of English higher education providers’ financial sustainability, but it’s also not especially surprising to anyone who has been following the sector’s fortunes over the past few years. While Office for Students (OfS) director of regulation Philippa Pickford is quick to offer reassurance that the sector as a whole is “healthy” and that “liquidity on average remains strong” fully 40 per cent of providers are forecasting a deficit in 2023-24.

Although most providers are forecasting recovery from 2024-25, as the regulator drily observes, the projected financial position “can only be relied on to the extent that those forecasts are credible.” A lot of that expected recovery seems to reply on the probability of growing the numbers of international students by, in aggregate between 22-23 and 26-27, 18 per cent for EU and 36.2 per cent for non-EU and, apparently, charging them more, as well as demographic-busting projections of growing home student numbers by nearly a quarter (23.9 per cent).

On current recruitment trends, which are set out in the report, something very material would have to change for those numbers to be realised. This is not, let’s be very clear, that university finance chiefs have been indulging in some banned substances while putting the numbers together – it’s just that the collective impact of each provider being a little bit optimistic is that the sector as a whole looks like it’s operating in cloud cuckoo land. The implication, set out in an accompanying OfS insight brief on navigating financial challenges in HE, is that many providers will need to take more difficult steps to secure their sustainability than they would like to – including bringing in the regulator to help manage the risks to students’ interests from inevitable reductions in spending.

Risky business

There have been some dicy moments for sector financing over the last decade, with worries over the fallout from Brexit, the impact of the Covid-19 pandemic, and pensions liabilities – yet most universities are still plugging on. So why is this crisis any different? At this point it is the scale and systemic nature of the issues affecting university finances that point to a need for early action rather than waiting for the storm to pass and hoping that future economic cycles will bring better luck.

OfS has identified a number of key risks to providers’ financial sustainability.

Inflation impacting both overall costs, and eroding the unit of resource (ie the undergraduate home fee, currently frozen at £9,250). The gradual effect of inflation has tended to encourage universities to seek modest efficiencies in undergraduate provision while expanding revenue-generating activities (like international recruitment) – but at some point, a strategy like this stops working either because the current model has been cut too far to be viable, or the revenue dries up, or both.

Exposure to reliance on international fee income – a risky source of income because despite the high appeal of the UK as a study destination, as we’ve seen numerous times, government policy in this area is not especially predictable, nor are the global conditions for international education. The UK remains very dependent on a flow of Chinese students, especially since recent restrictions to international student dependants have tended to hit applications from the countries the UK was trying to diversify its intake with – particularly India and Nigeria.

Investment in facilities and carbon reduction. Capital investment might be derided as being about “shiny buildings” but we’re well beyond the point now where fewer glass atriums will solve the sector’s financial problems. Capital investment is about future capacity, the quality of the learning and research environment, and managing environmental impact. Lack of investment now only stores up problems in the form of infrastructure debt for the future – something the whole UK is currently suffering from.

The impact of rises in the cost of living on students and staff, with students requesting additional financial and wellbeing support, and staff advocating for pay increases to meet their own financial challenges.

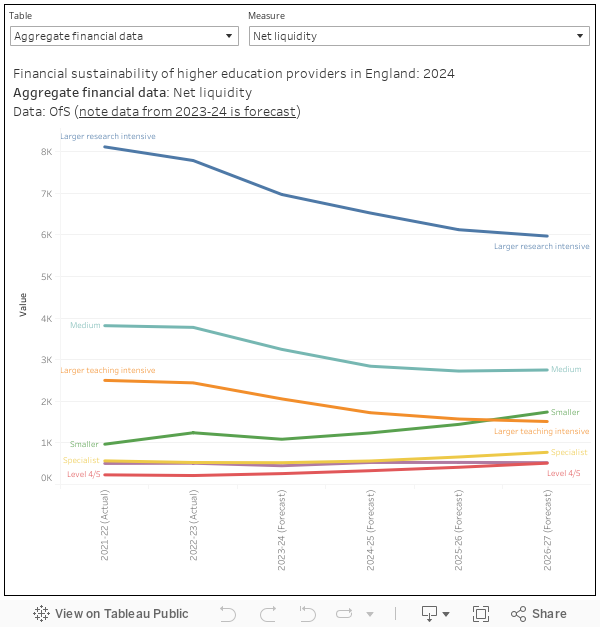

Data provision

There’s a suite of accompanying data, which DK has knocked up a handy visualisation for:

Scenario planning

That OfS has gone to the trouble of setting out alternative scenarios in which recruitment doesn’t bounce back as spectacularly as the sector seems to hope it will shows that the regulator is very worried indeed that many providers are not taking adequate measures to secure their institutions against the prospect of things not getting much better over the next five years.

These scenarios model at sector level – recognising that changes to student recruitment patterns would affect different institution to very different degrees, in a context where the extent to which an institution has levers available to it to adapt to a sudden change in recruitment is also highly variable.

One looks at a scenario of student numbers holding flat at 2023 levels, which would remove more than £3bn from current annual income projections by 2026-27 and push an estimated 64 per cent of providers into deficit.

A second scenario looks at a reduction in entrants of 11 per cent per year from 2024-25, resulting in a net annual projected income reduction of £4.5bn and 75 per cent of providers in deficit.

A third nightmarish but quite unlikely scenario projects the impact of a reduction in 35 per cent of entrants annually from 2024-25, resulting in an annual net loss of in projected income of more than £9bn, and 89 per cent of providers in deficit.

And a fourth equally nightmarish and if some politicians were to get their way, all too feasible, scenario projects what would happen if UK student recruitment stayed the same but international entrant declined annually by 22 per cent: a £9.7bn reduction in income against forecasts, and potentially deficits in 84 per cent of providers. This one, though scary, might actually be quite helpful in adding to the sector’s case on the international visa regime.

The implication here is that universities themselves need to be war gaming scenarios like these and have plans in place for what they would do – making mature judgements about the plausible impact on their institution and in some cases taking early action to reduce the likely consequences should those scenarios materialise. From what we hear many are already doing this work – we should be wary of reading across from what an institution will say in public to what it thinks in private, but where they are not, the regulator emphasises, it’s time to start confronting the unpalatable reality.

Yet while OfS is urging prudence on the sector, it is also spelling out very clearly the broader impacts of the steps providers will almost certainly need to take, lest there be any doubt that this challenge goes well beyond being a problem for vice chancellors and not the wider health of the nation.

Advocating good risk management to ensure institutional survival is one thing, but the plain fact is that if providers of higher education spend less money on fewer things there will be impacts on student choice and experience, the skills available, the research that is funded, and the ability of universities to contribute to regional economic growth and wellbeing. Impacts that will at some point require public investment to recover from.

The University sector is bloated. It is producing far too many graduates with no greatly improved job prospects , and only a great big debt to show for their efforts. We need to cap numbers to around 15-20% of the population attending HE and then Govt subsidy can be spread less thinly. Creation of our next workforce should involve far more on the job training rather than an abstract academic degree course. Some Universities should convert to mainly providing degree apprenticeships, but many others are going to have to close.

Agree entirely. The proposed growth in the knowledge economy, an argument used to sustain expansion in the sector, was simply overstated. As a result, we ended up supplying too many graduates with skills that the labour market did not value. A structural change along the lines above could work – a different balance of vocational and non-vocational routes could help us fund more social mobility across the board, and secure better outcomes.

@Paul Wiltshire If you look at the percentage of 25-34 year-olds with tertiary education, the OECD average is 47%. Capping at 15-20% would give the UK one of the lowest HE participation rates in the developed world.

Yes. Let’s all reduce the number of highly skilled, trained and educated folks in our economy – that will be a good thing, right? Have a suspicion, these people aren’t talking about ‘their’ kids/grandkids though.

Note Australia, Canada and others who are actively trying to grow the number of graduates in the economy. Where do you think the labour market is moving to? Less skilled?

More educated population don’t tend to vote for right wing governments, the government has had a dislike of universities since we all put up fees to the max – and the very existence of the post 92s has been a source of pain for the daily mail – so their will be no immediate help for the sector and many a tory thinking the current situation is a dream come true.

What about research and civic contribution? In some parts of the country Universities are among the largest employers, so letting them close would have massive long term impact. I do see a future with fewer institutions but thinking that mergers are likely to start happening in the not too distant future. Better that than a skilled workforce with no jobs surely?

One way to mitigate this longer term is for the sector to work together and create its own vision for the future (no point waiting for the government on this) whether that is at regional or national level it has to be better than the potential to loose around 75% of the sector and its associated benefits.